How we source rates and rate trends

Rates based on market averages as of Apr 19, 2026.Product Rate APR 30-year Fixed Refinance 6.26% 6.28% 30-year Fixed Jumbo Refinance 6.78% 6.80%

Refinancing your mortgage can be an effective way to lower your monthly housing costs. Plus, with interest rates continuing to come down from their late 2023 peak, an increasing number of homeowners are finding that today’s 30-year fixed refinance rates are lower than what they’re currently locked into.

The process of refinancing is simple: you take out a brand new loan with a new interest rate and monthly payment, which replaces your current mortgage. You can even use a refinance to tap into your property’s built-up equity and use those funds to consolidate high-interest debt, make home improvements, or simply have available for any other purpose you choose.

Government-Backed 30-Year Refinance Rates

How we source rates and rate trends

Rates based on market averages as of Apr 19, 2026.Product Rate APR 30-year Fixed Fha Refinance 5.60% 6.81% 30-year Fixed Usda Refinance 5.52% 5.66% 30-year Fixed Va Jumbo Refinance 5.72% 5.85%

In addition to conventional loans, there are several government-backed mortgage programs available to homeowners who qualify. Because they’re insured by the federal government, the 30-year refinance rates for these loans are typically lower than conventional alternatives.

FHA Refinances

FHA refinance loans are backed by the Federal Housing Administration and are designed for homeowners who may not meet conventional lending requirements.

According to FHA guidelines, borrowers can qualify with a credit score as low as 580; however, most lenders, including Refi.com, require a score of 620 or higher. FHA refinances typically allow a debt-to-income ratio up to 50%, and sometimes even higher with compensating factors.

All FHA refinances have an upfront mortgage insurance premium of 1.75% and an ongoing annual premium that typically ranges from 0.45% to 1.05%, depending on your loan size and loan-to-value ratio.

VA Refinances

VA refinances are insured by the U.S. Department of Veterans Affairs and are available to eligible veterans, active-duty servicemembers, and eligible surviving spouses. VA loans tend to have some of the lowest interest rates on the market, with flexible qualification requirements that can vary from lender to lender.

Borrowers refinancing through the VA program will incur a funding fee ranging from 0.5% to 3.3%. However, applicants with a service-related disability may qualify for a funding fee exemption.

USDA Refinances

USDA refinances are available only to homeowners with an existing USDA loan. These loans feature a 1% upfront guarantee fee and an annual fee of 0.35%, similar to new USDA loans.

Interest Rates by Loan Term

Many homeowners – especially those who are only a few years into their loan – refinance their loans back to a 30-year term. However, there are other mortgage options available for borrowers who want to reduce the length of time that they’ll pay on their home. Common alternatives include terms of 10, 15, 20, and 25 years.

Because you’re repaying the loan over a shorter period of time, these mortgages will come with higher payments than a 30-year fixed refinance. On the other hand, interest rates for shorter-term mortgages tend to be lower, and the reduced number of payments means that you’ll save on total interest costs over the life of your loan.

How we source rates and rate trends

Rates based on market averages as of Apr 19, 2026.Product Rate APR 15-year Fixed Refinance 5.34% 5.38% 20-year Fixed Refinance 6.09% 6.12% 30-year Fixed Refinance 6.26% 6.28%

30-Year Refinance Pros and Cons

As with any refinance, you should weigh the pros and cons. Here’s a quick look:

| Pros | Cons |

| Lower monthly payments than shorter-term loans | Higher interest rates than shorter-term loans |

| Practical option for cashing out built-up equity | Greater lifetime interest costs due to the 30-year term |

| Easier to qualify for if you have other existing debts | Building home equity takes more time |

| Ability to make extra payments to reduce your balance faster | Resetting the clock means paying on your home longer |

Let’s take a look at these in further detail.

The Benefits of a 30-Year Refinance

- Lower Monthly Payments: Because you’re repaying the loan over a 30-year period, your monthly payments will be lower than with a shorter repayment schedule, such as 15 or 20 years.

- Cashing Out Equity: Opting for a 30-year refinance makes payments more manageable when you’re doing a cash-out refinance and increasing the size of your mortgage.

- Easier to Qualify For: Because of lender debt-to-income ratio limits, the lower payments associated with a 30-year refinance make qualifying easier – especially for borrowers who have other existing debts.

- Flexibility to Reduce Your Balance Faster: Choosing a 30-year loan doesn’t prevent you from making additional payments towards your principal balance. This can help pay off your loan sooner and save you on overall lifetime interest costs.

Cons of a 30-Year Refinance

- Higher Interest Rates: Because of the longer term, 30-year fixed refinance rates are higher than for mortgages with shorter repayment periods.

- Greater Lifetime Interest Costs: Since you’re making payments for longer, 30-year loans have higher lifetime interest costs compared to shorter-term mortgages. In some cases, refinancing can increase finance charges over the life of the loan – especially when resetting the term.

- Slower to Build Equity: During the early years of your loan, very little of your payments go towards the principal balance, meaning you’ll build equity slowly.

- Longer to Pay Off Your Home: Doing a 30-year refi will reset the payment clock and keep you owing on your home for longer. This can be disadvantageous for borrowers who are already many years into their current loan.

Types of 30-Year Refinances

Most loan programs – whether conventional or government-backed – offer multiple types of 30-year refinances, each designed to fit different borrowing needs.

Rate-and-Term Refinance

A rate-and-term refinance allows you to obtain a new interest rate and loan term – such as 30 years – without adjusting the amount that you owe. Depending on the mortgage program you choose, you’ll likely need between 3% and 5% equity to qualify to refinance.

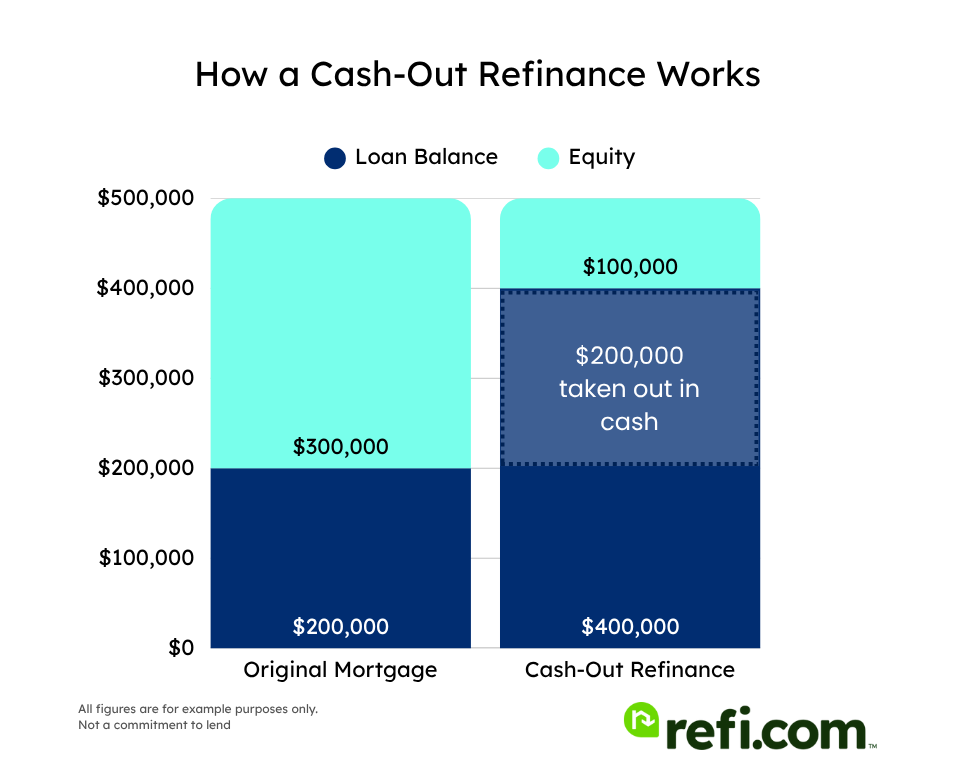

Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a new, larger loan, with the difference – minus closing costs – disbursed to you as part of the closing process.

The funds from a cash-out refinance can be used in any manner you choose. For conventional and FHA cash-outs, lenders typically limit borrowing to 80% of your home’s appraised value, meaning you’ll need to keep about 20% equity remaining after taking cash out. The VA allows cash-out refinances up to 100% of the appraised value, though most lenders cap this at around 90%.

Streamline Refinance

A streamline refinance is a unique type of rate-and-term mortgage offered through the FHA, VA, and USDA. With a streamline refi, you can generally refinance without needing to obtain a new appraisal, reverify your income, or undergo a detailed credit check. This generally translates into a simpler and faster refinancing process.

How to Refinance Into a 30-Year Term

Looking to replace your current loan with a new 30-year mortgage? Here are the six key steps that you’ll encounter along the way.

1. Identify Your Purpose for Refinancing

What is the primary goal that you hope to achieve by refinancing? Are you looking to reduce your interest rate, extend your loan term to lower your payments, or tap into your equity and receive a lump sum of cash?

2. Seek Preapproval With Three or More Refinance Lenders

Shopping around with multiple lenders can help you secure the best possible rate and closing costs. Be sure to seek preapproval with at least three different mortgage companies before deciding which one you want to work with.

3. Compare Interest Rates, Closing Costs, and Other Differences

Once you’ve received multiple mortgage quotes, compare them based on the factors that are most important to you. For some homeowners, this may mean securing the best interest rate, while others may be looking for the lowest possible upfront closing costs.

Keep in mind that loan offers are negotiable, and you may be able to use the most favorable quote to get the other lenders to compete to earn your business.

4. Apply With Your Preferred Mortgage Company

After you’ve decided which mortgage company you want to work with, the next step is to formally apply for your refinance. You may need to submit additional documentation, although you’ll have already provided the majority of the paperwork during the preapproval stage.

5. Respond Promptly During Underwriting

Loan underwriting begins after you’ve submitted your refinance application. At this point, the lender’s underwriters will take a more thorough look at your finances and evaluate your creditworthiness and overall level of risk. During underwriting, be sure to respond promptly to document requests from your loan team to avoid delaying the final approval.

6. Close On Your New Loan

Once the underwriting team has given the “clear to close” on your mortgage, the final step is to attend the closing – often handled remotely – where you’ll sign all of the loan paperwork. After closing, you’ll have officially completed your refinance. If you’re cashing out equity, you’ll receive the funds approximately three days after closing.

Understanding Market Averages

The numbers you see when looking at current 30-year fixed refinance rates are overall market averages and not necessarily indicative of the interest rate you’ll receive from any specific lender.

These averages are calculated by surveying a variety of different mortgage companies based on a consistent customer profile with a specific credit score, loan-to-value (LTV) ratio, loan amount, and other relevant factors.

Keep in mind that the actual refinance rate offered to you will vary based on your financial profile, individual borrowing needs, and the lender and loan product that you choose.

30-Year Refinance Conventional Eligibility Requirements

While government-backed loans may be better for some homeowners, the overwhelming majority of mortgages issued are conventional. These types of loans typically conform to the guidelines established by Fannie Mae and Freddie Mac.

In order to qualify for a 30-year conventional refinance, you will generally need to meet the following eligibility requirements:

- Credit Score: 620 or higher

- Debt-to-Income Ratio: 50% or lower

- Loan-to-Value Limits: Up to 97% in some cases for rate-and-term refinances; up to 80% for cash-out refinances

- Income Verification: Verifying your income typically involves providing two months of recent pay stubs, two years of W-2 forms, and two years of filed and accepted tax returns. Self-employed homeowners will have other requirements.

- Appraisal: Full professional appraisal required for most refinances

- Closing Costs: Generally 2% to 5% of the total amount borrowed

Should You Refinance Into a 30-Year Mortgage?

Refinancing your existing home loan with a 30-year fixed-rate mortgage can be a wise decision for borrowers who are able to lower their interest rate or reduce their monthly payments. It can also be a great way to tap into equity to fund home improvements or consolidate high-interest debt.

Keep in mind, though, that a 30-year refinance will reset the clock on your loan, meaning you’ll be making payments longer and may pay more in lifetime interest costs. Despite these disadvantages, refinancing with a 30-year mortgage remains a practical strategy in many scenarios.

Ready to begin refinancing your mortgage? Apply with Refi.com today!