- You don’t have to refinance to access your home equity. Options like HELOCs, home equity loans, home equity investments, and reverse mortgages let you tap equity while keeping your current mortgage intact.

- HELOCs and home equity loans are second mortgages — ideal if you can manage another monthly payment and want flexible or predictable terms.

- Reverse mortgages are available to homeowners 62 and older, offering cash without monthly payments — but the loan comes due when you move out or pass away.

- Home equity investments provide a lump sum with no monthly payments or interest but require sharing future home value gains when you sell.

Equity is one of the biggest perks of homeownership. As you pay down your mortgage or your home increases in value, you build equity — and with it, long-term financial strength. Equity boosts your net worth, creates opportunities for future moves, and can even help build generational wealth.

But equity can also be a financial resource in the here and now. You can use it to renovate your home, cover education costs, or tap it in an emergency for things like medical bills or car repairs.

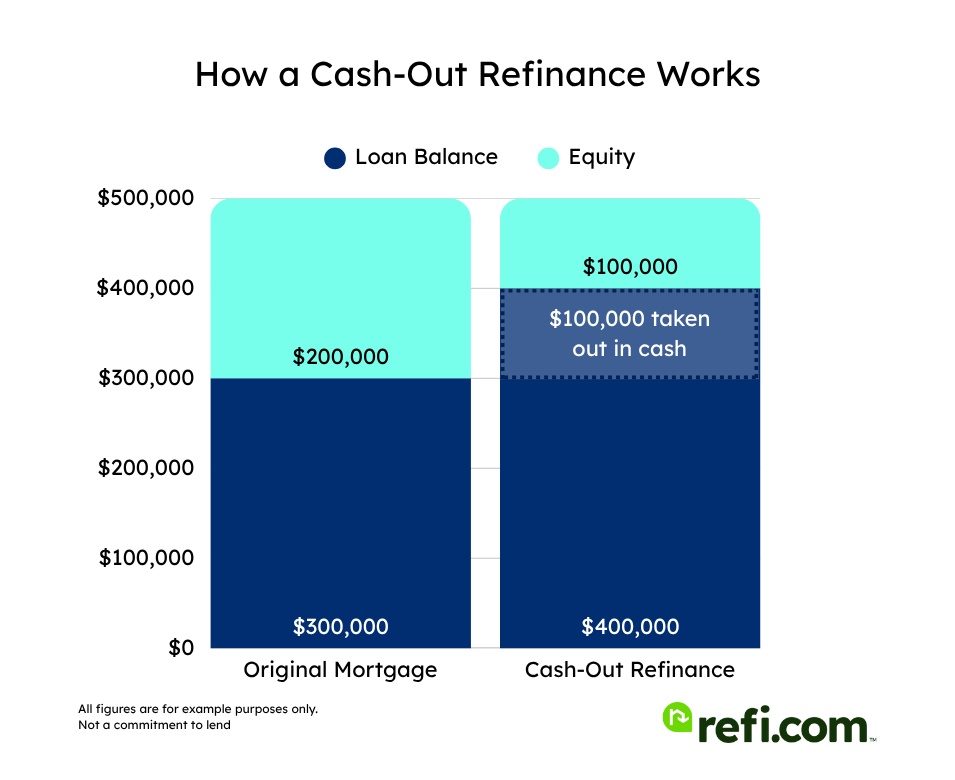

So how do you go about accessing that equity? A cash-out refinance is one common option — but it’s not always the best fit, especially when interest rates are high, or you’re hesitant to restart your loan term and pay new closing costs.

Fortunately, refinancing isn’t your only choice. Here’s what to know about how to get equity out of your home without replacing your current mortgage.

Can You Take Equity Out of Your Home Without Refinancing?

Yes — and there are several ways to do so.

One way is by taking out a second mortgage. This is a separate loan secured by your home that exists alongside your primary mortgage. The two most common types are home equity loans and home equity lines of credit (HELOCs), both of which let you borrow against the equity you’ve built without replacing your current loan.

You can also use a home equity investment — a relatively new tool that lets you tap your equity without taking on monthly payments or interest.

Finally, if you’re age 62 or older, you may be eligible for a reverse mortgage, which lets you convert equity into cash without monthly payments. The loan is repaid when you move out, sell the home, or pass away.

Here’s a quick snapshot of how these options compare (note that terms often vary by lender):

| Feature | Cash-Out Refinance | HELOC | Home Equity Loan | Home Equity Investment (HEI) | Reverse Mortgage |

| Payment Structure | New mortgage payment | No payments while living in the home | Fixed monthly payments | No monthly payments | No payments while living in home |

| Interest Rates | Fixed or variable | Variable (often) | Fixed (usually) | N/A | Fixed or variable |

| Rate Comparison | Can be the lowest, especially in a low-rate environment | Typically higher than mortgage rates | Higher than first mortgage, but lower than unsecured loans | No interest rate | Usually higher than conventional mortgage rates |

| Loan Term | 15–30 years | 10-year draw + 10–20-year repayment | 5–30 years | Typically 10–30 years or upon sale | Due upon sale, move-out, or death |

| Funds Received | Lump sum at closing | Withdraw as needed | Lump sum | Lump sum | Lump sum, monthly, or line of credit |

| Upfront Costs | 2–5% of the loan amount | Often lower; may include annual fees | Moderate closing costs (1–5%) | May include service or origination fees | High — usually 2–5% of home value |

| Foreclosure Risk | Yes | Yes | Yes | No | Yes |

| Best For | Lowering rate + getting cash | Ongoing access to cash | One-time major expenses | No-payment flexibility + large equity | Seniors needing cash without selling |

Home Equity Line of Credit (HELOC)

A home equity line of credit, or HELOC, is a type of second mortgage — an additional loan on top of your existing mortgage, as opposed to a refinance, which replaces it.

With a HELOC, a portion of your home equity is converted into a revolving line of credit you can draw from as needed over a 10-year period. It works similarly to a credit card — you can use as much or as little of the credit line as you’d like, and you only pay interest on what you borrow.

This makes HELOCs especially useful if you need funds over an extended period or aren’t sure of the total cost upfront — like an ongoing renovation or long-term medical treatment.

The downside is that HELOCs usually have variable rates, meaning your payment could change over time. They also add a second monthly obligation to your budget.

A HELOC tends to make more sense than a cash-out refinance when you already have a low rate on your primary mortgage and don’t want to give it up. A refinance may be better if it would meaningfully lower your rate or payment.

Home Equity Loan

A home equity loan is another type of second mortgage taken out alongside your existing loan. Unlike a HELOC, you receive a single lump-sum payment at closing rather than a revolving line of credit.

Home equity loans typically come with fixed interest rates, so your payment stays predictable. Terms of up to 30 years are available. The tradeoff is a second monthly payment and — like any mortgage — your home is at risk of foreclosure if you can’t keep up with payments.

A home equity loan is usually the better choice when you want to preserve your existing mortgage terms and rate, and when you know exactly how much you need to borrow. A refinance may make more sense if you’re concerned about managing two payments or if you could qualify for a lower rate than you currently have.

Home Equity Investment (HEI)

A home equity investment lets you sell a stake in your home’s future value in exchange for a lump-sum payment today. There are no monthly payments and no interest — but when you eventually sell the home, the investor takes a share of the proceeds.

Home equity investments are completely separate from your mortgage — no refinancing, no second monthly payment, and no additional loan on your title.

The major upside is the potential to access large amounts of cash (some companies offer up to $600,000) without adding financial stress to your monthly budget. The downside is that if your home appreciates significantly, you could end up giving up much more than you originally received.

If you’re weighing this against a refinance, consider your current mortgage terms, how much you need, and your timeline. If you need a large sum, can’t absorb a second monthly payment, and don’t plan to sell for some time, a home equity investment may be the better fit.

Reverse Mortgage

A reverse mortgage lets homeowners age 62 and older borrow against their home equity and receive funds as a lump sum, monthly payments, or a line of credit — with no required monthly repayment as long as you live in the home. The balance comes due when you move, sell, or pass away.

When the homeowner passes away, heirs typically repay the loan by selling the home. If the home sells for more than the loan balance, the heirs keep the difference. If it sells for less, they’re not responsible for the shortfall — reverse mortgages are non-recourse loans, meaning the lender cannot pursue other assets to recover the balance.

Reverse mortgages can be a helpful income tool for retirees who want to stay in their homes. Just keep in mind that upfront fees tend to be high, and the loan balance grows over time, which can reduce the equity left for heirs.

When Refinancing Is the Better Option

Despite the variety of alternatives, a cash-out refinance can still be the right move in the right circumstances. Consider refinancing if:

- You can lower your interest rate. If market rates have dropped since you got your mortgage — or your credit score has improved — refinancing could mean meaningful savings over the life of the loan.

- You want to change your loan term. Refinancing lets you shorten your term to pay off your home faster, or extend it to reduce your monthly payment.

- You need to add or remove a borrower. Divorce, marriage, or shifting financial responsibilities may require a change to who’s on the mortgage — and refinancing is typically the only way to make that happen officially.

- You want to consolidate debt. A cash-out refinance lets you roll high-interest debt into a lower-rate mortgage, simplifying payments and potentially reducing your monthly payments.

- You’d rather manage one payment. Unlike a HELOC or home equity loan, a cash-out refinance keeps everything in a single monthly payment.

Even in a higher-rate environment, refinancing can make sense depending on your goals. If you’re unsure, run the numbers or talk to a mortgage professional.

Things to Consider Before You Tap Your Home Equity

Before committing to any home equity product, work through these questions.

1. How much equity do you actually have?

You may have more — or less — equity than you think. Most lenders require you to leave 15% to 20% equity in the home after borrowing, so understand what’s actually accessible before you get too far along.

2. What will you use the funds for?

Equity is a smart tool for home improvements or debt consolidation — uses that can raise your home’s value or reduce your interest burden. Using it for short-term wants or nonessential expenses could put your finances at unnecessary risk.

3. Can you handle an extra monthly payment?

HELOCs and home equity loans add a second monthly obligation. Make sure your budget can absorb it — especially if you’re considering a product with a variable rate.

4. How long will you stay in the home?

If you plan to move in the next few years, refinancing may not be worth the closing costs, and some products like home equity investments or reverse mortgages may not have enough time to deliver their full benefits.

5. What are the tax implications?

Interest on a HELOC or home equity loan may be tax-deductible — but only if the funds are used to “buy, build, or substantially improve” the home. If you plan to use the funds for something else, consult a tax advisor first.

6. Are you comfortable with the risk?

Tapping equity means putting your home on the line. Missed payments on second mortgages can lead to foreclosure, and with home equity investments, your future proceeds from selling the home may be significantly reduced.

How to Tap Home Equity Without Refinancing

Ready to move forward? Here’s how to proceed:

1. Calculate Your Equity

Subtract your current mortgage balance from your home’s estimated market value. For example, if your home is worth $400,000 and you owe $250,000, you have $150,000 in equity.

But keep in mind: most lenders require you to leave at least 20% equity in the home after borrowing. On a $400,000 home, that’s $80,000 — meaning you could potentially access up to $70,000 (before closing costs).

The actual amount will vary based on your lender, credit score, debt-to-income ratio, and the product you choose.

2. Assess Your Finances

Review your monthly income, expenses, and existing debts. Know how much you need, how you’ll use it, and whether it makes sense to borrow a bit more as a buffer for unexpected costs.

3. Choose Your Equity Product

Pick the tool that best fits your goals. HELOCs offer flexibility; home equity loans provide a lump sum with predictable payments; home equity investments offer cash with no monthly payment in exchange for a share of future appreciation.

4. Apply with a Lender

Shop around and compare offers. Look at interest rates, fees, repayment terms, and how each option would affect your monthly cash flow. Don’t hesitate to negotiate on origination fees or closing costs. Have your documentation ready — income statements, tax returns, and asset details — to streamline the process.

The Bottom Line

There’s more than one way to access your home equity — and refinancing isn’t your only option. From HELOCs and home equity loans to home equity investments and reverse mortgages, each product has unique advantages depending on your age, equity position, financial goals, and risk tolerance.

Of course, a cash-out refinance still has its place — especially if it helps you lock in a better rate, consolidate debt, or adjust your loan term.

Ready to explore your options? Start your home equity application with Refi.com today — or see if a refinance makes more sense for your situation.

More Reading

Want to learn more about tapping into your home equity? Check out these articles: